Are you ready to understand why property management is a key control?

Robert starts by explaining that property management is essential for making real estate profitable, but it’s not something he personally enjoys. That’s why he teamed up with Ken McElroy, author of The ABC’s of Real Estate Investing, whose company specializes in property management.

He recommends that if we're interested in learning more about property management and how it can increase real estate value, check out the books and resources from The Rich Dad Company, created by Ken.

Robert tends to avoid stocks and mutual funds because he can't control things like CEO salaries and bonuses. For instance, Home Depot’s former CEO, Robert Nardelli, was paid $38 million a year plus big bonuses, even when the company was struggling. This high pay is one of the reasons why Robert prefers real estate over paper assets, which are often managed by people more focused on their own financial security than that of the investors.

When it comes to financial intelligence, the third area to focus on is liabilities.

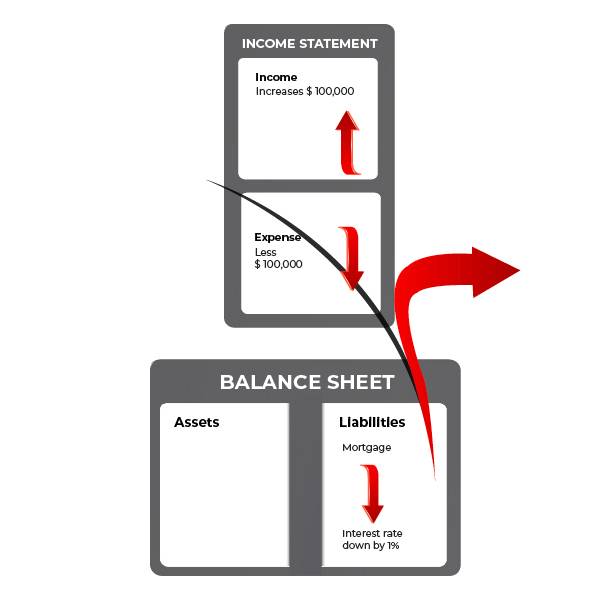

Robert’s 300-unit apartment complex had a mortgage rate of 4.95%, which increased its value. By adding a second mortgage at 6.5%, they created an average blended rate of about 5.5%. A lower interest rate can have a huge impact on increasing profits.

For example, saving just 1% on a $10 million mortgage results in an extra $100,000 in income each year. Reducing debt and lowering interest rates helps increase profits as well.

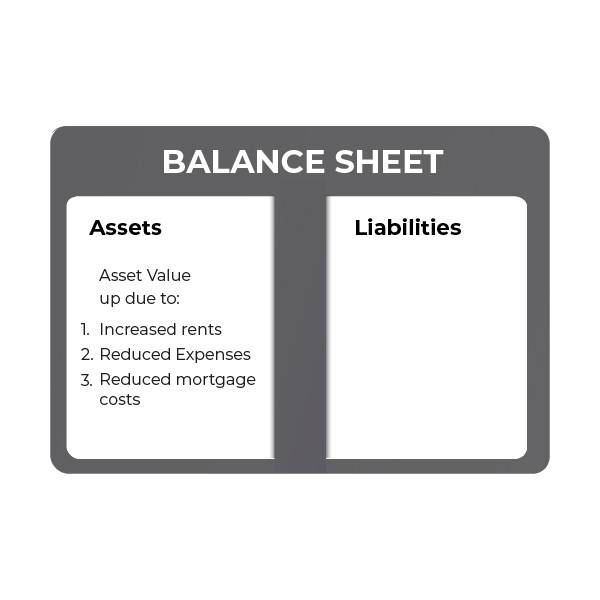

The last part of financial intelligence is about the asset column.

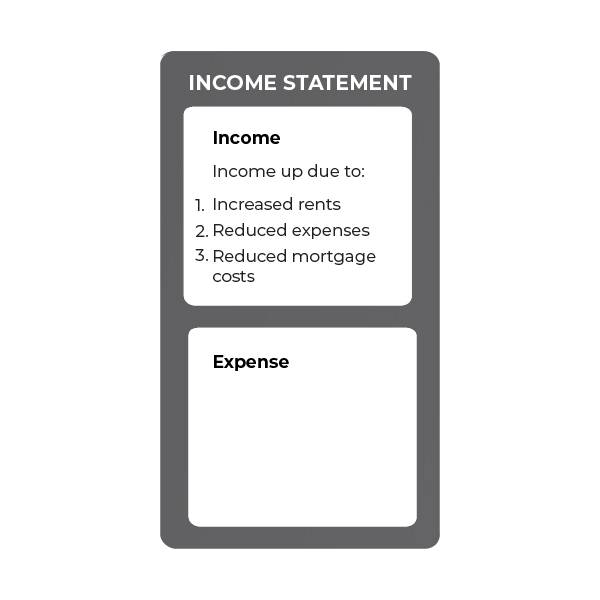

By increasing rents, cutting costs, and reducing debt or interest, you can increase a property’s value. By carefully controlling these factors and getting the right numbers, you're leveraging your position and applying important financial knowledge.

What is "bobbing for apples"?

With the ups and downs of the stock market, many investors feel like they’re playing carnival games—fun, but not a reliable way to make long-term gains. Instead of constantly watching the price changes of stocks or mutual funds, Robert wants to take control of his financial future. By learning how to manage income, expenses, debt, and investments, he can steer his own financial path.

As an investor, he can’t control things like savings, stocks, bonds, or mutual funds.

Lastly, Robert shares seven important points to keep in mind before using higher forms of leverage and control!